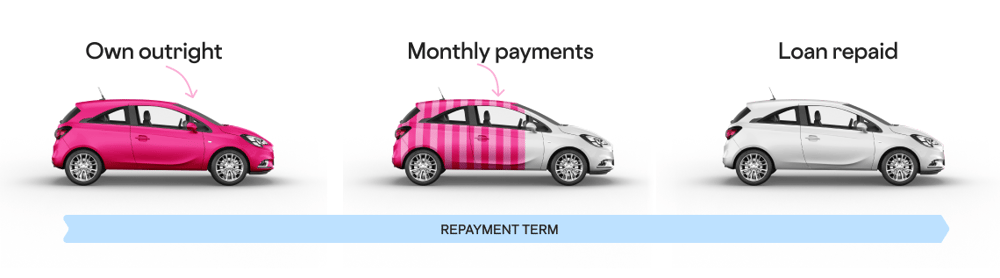

HP vs PCP is the big debate in car finance. They’re two of the most popular ways to spread the cost of buying a new or used car and have many...

Our first 1,000 customers will be driving off happy with an awesome Carmoola swag box 😎

Download the Carmoola App

Cruise through car finance and pay for your car with a plan that suits you.

Scan the QR code or click the pink button to get the Carmoola app

Rates from as little as 6.9% APR, representative 15.7% APR