.webp?width=832&height=592&name=customer-support%20(1).webp)

Car Finance

Car Finance

Cars & Gadgets

Cars & Gadgets

Car Maintenance

Car Maintenance

Tips & Advice

Tips & Advice

News

News

Road Trips

Road Trips

Pop Culture

Pop Culture

.webp?width=400&height=285&name=online-shoppers-with-dog%20(1).webp)

.jpg?width=500&height=356&name=Vintage%20car%20going%20to%20an%20old%20town-1%20(1).jpg)

Written by

Verified by

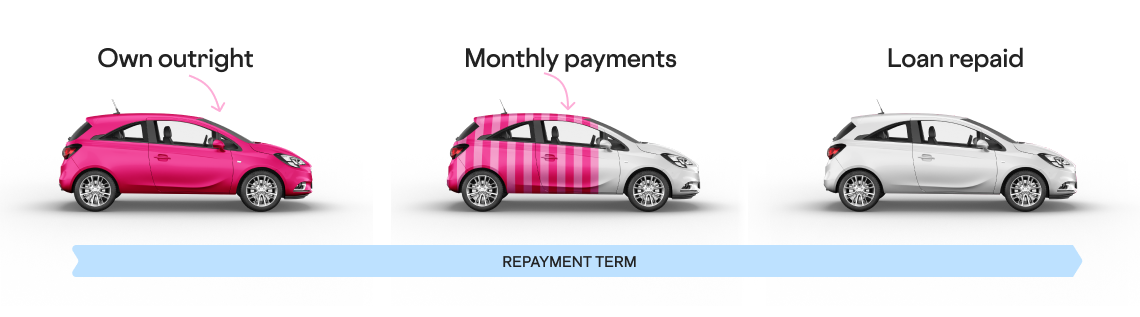

In a nutshell, car finance is when you borrow money from a lender to buy a new or used car. You usually put down a deposit and then make monthly payments to repay the money, with interest, over a fixed amount of time. Think of it like a mini mortgage for buying a car.

A car finance agreement typically lasts between one and six years. At the end of this time, you might have the option to own the car outright, or swap it for a new one, or hand it back and walk away, depending on what type of car finance you’ve got.

What are the different types of car finance?

Car finance is an umbrella term that covers a few different types of borrowing. Here’s how they work:

Personal Contract Purchase (PCP)

You pay a deposit upfront, then make fixed monthly repayments for a set period. At the end, you can make a big one-off payment (called a balloon payment) to own the car, or you can hand it back, or you can use any positive equity you’ve built up as a deposit on another car. Personal Contract Purchase is great if you like to change your car every few years, and you’re not bothered about owning the car.

Hire Purchase (HP)

Like PCP, you pay a deposit followed by fixed monthly payments. At the end of the term, you can pay a one-off Option To Purchase fee (usually £100 - £200, but just £1 with Carmoola) to become the legal owner. Hire Purchase tends to be a good option if you’re happy to commit to a car for a longer time.

Personal Contract Hire (PCH)

Also known as leasing, PCH is like a long-term car rental. You put down a deposit, then make monthly payments for two to four years. You have to stick to annual mileage limits, and keep the car in good condition, otherwise you’ll have to pay extra fees. At the end of the agreement you hand it back to the lease company - there isn’t usually an option to own the car.

Personal loan

You borrow money from a lender, use the money to pay for the car, then repay the loan over a fixed term. Personal loans aren’t secured against the car, so you’re the legal owner from day one, and you’re free to do whatever you like with it - upgrades, long road trips, you name it. But, unsecured loans are more risky for the lender, so you’ll need a good credit score and a strong payment history.

Car subscriptions

A bit like leasing, but without the long term commitment. You typically pay a fixed monthly fee for a flexible month-by-month subscription. Car subscriptions are often only available on brand new cars, and tend to be more expensive than longer term leases. But, all the incidental costs are included so the only extra you have to pay for is fuel. It’s an ideal option if you want access to a car without a long-term commitment.

How much will finance cost me?

Well, that depends. Lots of things influence the cost of your car finance, including:

Loan amount

The amount your car is worth is one of the biggest things that influences your car finance repayments. The more the car is worth, the more you’ll pay each month.

Interest rate

The interest rate on your loan has a big impact on how much you’ll pay, both monthly and overall. You’ve got a better chance of being offered a lower interest rate if your credit score is in good shape.

Loan length

A longer term for your loan usually means lower monthly payments, but can add up to repaying more overall, because you’ll pay more in interest. A shorter term tends to come with higher monthly payments, but you’ll pay less in interest.

Extra fees

You might have to pay extra charges in a PCP or PCH agreement if the car is damaged beyond fair wear and tear when you return it, or if you’ve gone over the agreed annual mileage limit.

What is the best option for me?

There’s no right or wrong - the best car finance option for you will be the one that fits your budget, circumstances and preferences. To help you decide on the best option, ask yourself.

How are your finances looking?

Think about how much you can afford to repay each month - longer term agreements usually come with lower repayments, but could cost you more overall.

Do you have a deposit available?

Most car finance agreements tend to ask you for a deposit upfront - usually around 10% of the car’s value - but if you don’t have this kind of cash lying around, there are no-deposit deals available too. Borrowing money with a personal loan doesn’t need a deposit either, so this could be an option for you.

How’s your credit score?

If your credit score’s in good shape, and you don’t have a history of missing payments, you could get a good deal on an unsecured loan, like a personal loan. On the other hand, if you need to work on your score, you might be better off with a secured loan like PCP or HP.

Do you want a new or used car?

Car subscriptions and PCH deals are usually only available on brand new cars, whereas you can use HP, PCP and a loan to buy a new or used car. If you like to switch things up and change your car regularly, PCP or a subscription might suit you. On the other hand, if you’re happy keeping the same car for a longer time, you could consider HP, a loan, or a lease.

Do you want to own the car?

If you dream of being your car’s legal owner, then PCH or subscriptions probably aren’t for you, as you’ll have to hand the car back at the end of the agreement.

How do you drive?

Long distance commuter who racks up a lot of mileage? You probably won’t want a finance agreement that comes with an annual mileage limit, like PCH or PCP. If you only use your car to pop to the shops or pootle around locally, a mileage limit might be easy to stick to.

What are the pros and cons?

Like anything money-related, it’s super important to consider the pros and cons of a car finance agreement before you jump in and sign on the dotted line. Every deal is different, but here are the general benefits and drawbacks to weigh up:

Pros

- Car finance can make it more affordable to drive newer cars

- You may have more choice of cars within your budget

- If you like to change your car more regularly, some finance options will let you do this

Cons

- You could end up in negative equity, where the amount you own on the loan is more than the car’s worth

- You might have to pay extra charges if the car is damaged, or if you go over the mileage limit

- Car finance is a legally binding contract, and a big commitment - make sure you understand what you’re agreeing to before you go for it

What are the top 5 used car websites in the UK?

Thanks to the internet, searching for a used car in the UK is easier than ever before. You can simply head online, visit a used...

Hire purchase or leasing? Key differences and what to choose

When you’re choosing between hire purchase and leasing, the key difference is whether you want to own the car or if you prefer...

Can you get car finance without a driving licence?

Yes, some lenders offer car finance without a driving licence, but Carmoola requires a full UK driving licence to complete an...