.webp?width=832&height=592&name=customer-support%20(1).webp)

Car Finance

Car Finance

Cars & Gadgets

Cars & Gadgets

Car Maintenance

Car Maintenance

Tips & Advice

Tips & Advice

News

News

Road Trips

Road Trips

Pop Culture

Pop Culture

.webp?width=400&height=285&name=online-shoppers-with-dog%20(1).webp)

.jpg?width=500&height=356&name=Vintage%20car%20going%20to%20an%20old%20town-1%20(1).jpg)

What is PCP finance?

PCP, or Personal Contract Purchase, is a flexible car finance agreement that allows you to spread the cost of a car over a convenient length of time, typically 2 to 6 years.

Lower fixed monthly payments than other finance options

Flexibility to purchase the car, return it or enter into another PCP agreement at the end

Potential for upgrading your car every few years

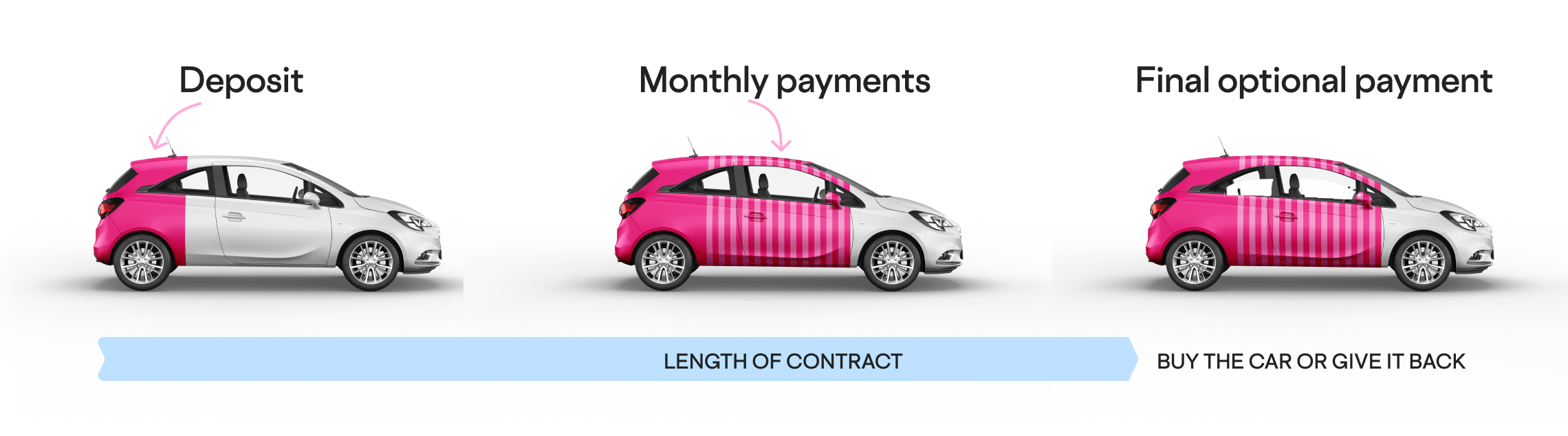

How does PCP finance work?

1. Pay an optional deposit upfront and decide on the mileage limit.

2. You make fixed regular monthly payments throughout the agreed term. You are not the legal owner until all sums due have been repaid.

3. As you come to the end of the term, you have the flexibility to either:

- Own the car outright by paying a lump-sum final balloon payment.

- Hand it back to the lender.

- Upgrade to a brand new car with a fresh PCP agreement.

The balloon payment covers your car’s depreciation and reflects its predicted value at the end of the contract – known as the Guaranteed Minimum Future Value (GMFV).

Compare PCP, HP and personal loans

|

Personal Contract Purchase (PCP) |

Hire Purchase (HP) |

Personal Loan |

|

|---|---|---|---|

|

No deposit required |

|

|

|

|

Car is yours at the end of the agreement |

Optional |

|

|

|

Fixed monthly payments |

|

|

|

|

No (final) balloon payment |

|

|

|

|

No excess mileage charges |

|

|

|

|

Secured against |

|

|

|

|

Available on Carmoola |

|

|

|

This table shows common agreement features. Check with the lender for specific terms.

Can I get PCP car finance?

You can apply for PCP (Personal Contract Purchase) car finance if you meet the basic eligibility criteria. Most lenders will look at a few key things, including:

Your credit history

Your income and affordability

Proof of identity and address

At least 18 or over

Your PCP journey start to finish

To apply for a PCP (Personal Contract Purchase) agreement, you'll need to provide some personal details such as your name, address, income, and employment status. The process usually includes a soft credit check to assess your eligibility. After that, you'll choose the car you want and go over the terms of the PCP agreement—this includes the deposit amount, monthly payments, and your options at the end of the term. Once everything is agreed upon, you sign the contract and you're good to go!

How does PCP work at the end?

When the PCP agreement comes to an end, you’ll have three main options: pay a final balloon payment to keep the car, return the car to the lender, or start a new PCP agreement with a different vehicle.

An example of how your PCP payments could look like

Example: Borrowing £10,000 over 48 months with a representative APR of 13.9% and a £0 deposit.

The monthly payment would be £208 for 47 months, followed by an optional final payment of £4,001, including a one-off Option to Purchase fee of £1. The total cost of credit would be £3,776, and the total amount payable would be £13,777.

Carmoola provides car finance directly as a lender. In cases where we can’t offer finance ourselves, we may act as a credit broker.

How it works

How it works

No sales calls or lengthy paperwork.

You only need our app, and a full

driving licence.

Still searching for your dream ride?

Browse thousands of cars from approved dealerships, and see your budget in seconds.

Let’s find my carWhy our

customers keep coming back 👋

I’m loving my new car life 🚗

Angelina Range Rover Evoque

Amazing efficiency and a professional way of financing. The paperless system is the top notch.

Biliat Range Rover Evoque

I bought my very own first car using Carmoola. They helped me out so much with the whole process.

Bethany Fiat 500

Easy to join. Thanks Carmoola, my dream has come true.

HoJing Toyota GT86

Carmoola is just the best, everything happened in minutes and their staff are simply the best. They made my experience perfect.

Kudzanai DS 3

Need help choosing car finance?

PCP vs HP car finance: what's the difference and which is better?

When you're choosing between a PCP or HP car finance, the decision often depends on whether you prefer lower monthly payments or...

2 Min Read

PCP vs leasing: Which is better?

If you’re looking into your options for car financing, it can be confusing. Personal Contract Purchase (PCP) and leasing both...

2 Min Read

How does personal contract purchase (PCP) finance work?

Personal Contract Purchase (PCP) is a popular way to finance buying a car without having to pay for it upfront. It allows you to...

2 Min Read

Our PCP finance FAQs

Here are the most frequently asked questions about how PCP works.

Got more questions? Head over to our FAQs page 👍

Does Carmoola offer Personal Contract Purchase finance?

Yes! We’ve launched PCP, so click here to Get A Budget and see if you’re eligible for HP, PCP, or both!

Can you leave your PCP agreement early?

Yes, you can end a PCP (Personal Contract Purchase) agreement early, but there are a few important things to consider. Depending on your contract and how you choose to exit the agreement, you may need to pay off part of the remaining finance in advance. You’ll also need to return the car to the lender, and you could be charged for any excess mileage or damage beyond what’s considered fair wear and tear.

It’s always best to check the specific terms of your PCP agreement so you know exactly what to expect.

Is PCP better than HP?

Whether PCP or HP is better depends on your individual circumstances. PCP offers flexibility with its end-of-term options, while HP has the benefits of no mileage allowance restrictions. Consider your financial circumstances, desire for flexibility at the end of an agreement and driving habits to determine which option suits you best.

Is PCP a good idea?

A Personal Contract Purchase (PCP) can be a smart choice if you like changing your car every few years, want lower monthly payments, and are comfortable not owning the vehicle outright during the term. It offers flexibility at the end of the agreement, whether that’s returning the car, trading it in, or paying the final balloon payment to keep it.

Can I get PCP with bad credit?

Yes, it’s possible to get a PCP (Personal Contract Purchase) agreement with bad credit (a low credit score), but it may be more challenging. Lenders will look at your credit history to assess the level of risk involved, and having a lower credit score could mean:

- You’re offered higher interest rates

- You might need to provide a larger deposit

- There’s a chance your application could be declined, depending on the lender’s criteria

That said, some finance providers specialise in offering options to people with less-than-perfect credit. It can help to check your credit report in advance, consider improving your score where possible, and be honest on your application.

At Carmoola, we aim to make car finance clear and accessible. We’ll let you know your eligibility quickly (without impacting your credit score) so you can see your options upfront.

Can I get PCP with no deposit?

Yes, you can get a PCP (Personal Contract Purchase) deal with no deposit, but it depends on the lender and your circumstances. Some finance providers offer zero-deposit PCP options, which means you won’t need to pay anything upfront, but your monthly payments may be higher as a result.

A no-deposit PCP can be a good option if you don’t want to tie up your savings or need to keep upfront costs low. Just be sure to check the total cost over the term of the agreement and make sure it fits your budget.

What happens if I go over my mileage?

If you go over your agreed mileage limit on a PCP (Personal Contract Purchase) plan, you’ll usually need to pay an excess mileage charge. This is a cost set by the lender, typically charged per mile over your limit, and can reach 15p per mile, but it can vary.

This charge only applies if you return the car at the end of the agreement. If you choose to buy the car by paying the final balloon payment, mileage won’t affect you in the same way.

To avoid unexpected costs:

- Try to estimate your mileage realistically when you take out the agreement

- Keep an eye on your usage during the term

At Carmoola, we’re upfront about mileage limits and costs, so you always know where you stand before you commit.

Is PCP bad for credit score?

Not at all. PCP (Personal Contract Purchase) isn’t bad for your credit as long as you manage the agreement responsibly. In fact, it can help improve your credit score if you:

- Make all your monthly payments on time

- Stay within the terms of your agreement

- Avoid taking on more credit than you can handle

However, like with any form of finance, missing payments or defaulting could negatively impact your credit file.

So while PCP itself isn’t bad for your credit, how you manage it matters. Keeping up with repayments shows lenders you’re reliable, which can boost your credit profile over time.

With the Carmoola app, you get a clear view of your monthly payments, so you always know where you stand.

What can I do if I am falling behind with PCP car finance payments?

If you're struggling to make your PCP payments, it's important to contact your lender as soon as possible. They may be able to offer assistance, such as extending the term of your agreement or reducing your monthly payments to help ease the pressure on your finances.

Can you modify a car on a PCP agreement?

Generally, you can’t modify a car on a PCP agreement, as some modifications may affect the car's value which is typically a risk that lenders are not willing to take on.

Outstanding help and support

Got a question? Our friendly, UK-based team is here from

8am - 9pm EVERY day, via WhatsApp, email, SMS or phone.